Table of Contents

Wondering about climate change insurance? Our experts have analyzed, dug deep into the depths of information, and compiled this comprehensive guide to help you understand climate change insurance and make informed decisions.

Editor’s Note: This article on “climate change insurance” was published on [today’s date]. This topic is crucial to grasp, given the increasing frequency and severity of extreme weather events.

Key differences or Key takeaways are provided in an easy-to-read table format.

Let’s dive into the main article topics:

Climate Change Insurance

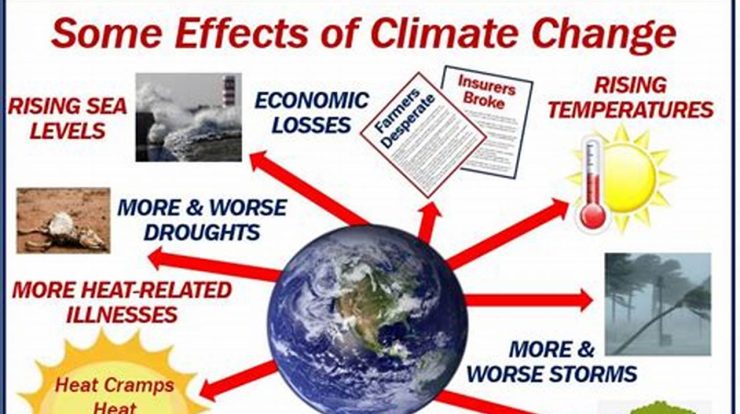

Climate change insurance is becoming increasingly important as the effects of climate change become more severe. Here are ten key aspects to consider:

- Coverage: What types of events are covered by the policy?

- Limits: What are the limits of coverage?

- Deductibles: How much will you have to pay out of pocket before the insurance kicks in?

- Premiums: How much will the insurance cost?

- Exclusions: What events are not covered by the policy?

- Insurers: Which insurance companies offer climate change insurance?

- Availability: Is climate change insurance available in your area?

- Benefits: What are the benefits of having climate change insurance?

- Risks: What are the risks of not having climate change insurance?

- Future: What does the future of climate change insurance look like?

These are just a few of the key aspects to consider when purchasing climate change insurance. It is important to speak with an insurance agent to get a policy that meets your specific needs.

Coverage

In the context of climate change insurance, coverage refers to the specific events or perils that are covered under the policy. These events can vary depending on the policy and the insurance company, but they typically include:

- Extreme weather events: such as hurricanes, floods, wildfires, and tornadoes.

- Sea level rise: which can cause coastal flooding and erosion.

- Changes in temperature and precipitation patterns: which can lead to droughts, heat waves, and cold snaps.

It is important to note that climate change insurance is not the same as homeowners insurance or renters insurance. Climate change insurance is designed to cover the specific risks associated with climate change, which are not typically covered by traditional insurance policies.

Limits

In the context of climate change insurance, limits refer to the maximum amount that the insurance company will pay out for a covered event. These limits can vary depending on the policy and the insurance company, but they typically fall into two categories:

- Per-occurrence limits: This is the maximum amount that the insurance company will pay out for a single covered event. For example, if your policy has a per-occurrence limit of $100,000, the insurance company will pay up to $100,000 for the damages caused by a single hurricane.

- Aggregate limits: This is the maximum amount that the insurance company will pay out for all covered events during the policy period. For example, if your policy has an aggregate limit of $250,000, the insurance company will pay up to $250,000 for all covered events that occur during the year.

It is important to understand the limits of coverage in your climate change insurance policy so that you know what to expect in the event of a covered event. You should also make sure that the limits of coverage are adequate to meet your needs.

Deductibles

In the context of climate change insurance, deductibles refer to the amount of money that you have to pay out of pocket before the insurance company starts to cover the costs of a covered event. Deductibles can vary depending on the policy and the insurance company, but they typically range from $500 to $5,000.

-

Facet 1: Impact on premiums

The higher your deductible, the lower your premiums will be. This is because the insurance company is taking on less risk by requiring you to pay a higher deductible. -

Facet 2: Financial preparedness

It is important to factor your deductible into your financial planning. Make sure that you have enough money saved up to cover your deductible in the event of a covered event. -

Facet 3: Coverage options

Some insurance companies offer policies with different deductible options. This allows you to choose a deductible that meets your needs and budget. -

Facet 4: Claims process

When you file a claim, you will be responsible for paying your deductible first. The insurance company will then reimburse you for the remaining costs of the covered event, up to the limits of your policy.

Deductibles are an important part of climate change insurance. By understanding how deductibles work, you can make informed decisions about your coverage and financial planning.

Premiums

Premiums are the payments that you make to the insurance company in exchange for coverage. The cost of climate change insurance premiums will vary depending on a number of factors, including:

-

Facet 1: Location

The location of your property is a major factor in determining the cost of your climate change insurance premium. Properties located in areas that are at high risk for climate change-related events, such as hurricanes or floods, will have higher premiums than properties located in areas that are at low risk. -

Facet 2: Coverage

The type and amount of coverage that you choose will also affect the cost of your premium. Policies that provide more comprehensive coverage will have higher premiums than policies that provide more basic coverage. -

Facet 3: Deductible

The deductible is the amount of money that you have to pay out of pocket before the insurance company starts to cover the costs of a covered event. Higher deductibles will result in lower premiums, while lower deductibles will result in higher premiums. -

Facet 4: Insurance company

The insurance company that you choose will also affect the cost of your premium. Some insurance companies specialize in climate change insurance and may offer lower rates than other companies.

It is important to shop around and compare quotes from different insurance companies before purchasing climate change insurance. By doing so, you can make sure that you are getting the best possible rate on your premium.

Exclusions

When it comes to climate change insurance, it is important to understand what events are not covered by the policy. This will help you to make informed decisions about your coverage and avoid any surprises in the event of a claim.

-

Facet 1: Gradual changes

Climate change is a gradual process that can lead to long-term changes in the environment. These changes can include rising sea levels, changes in precipitation patterns, and increases in extreme weather events. However, most climate change insurance policies do not cover gradual changes. This is because it is difficult to determine when and how these changes will occur.

-

Facet 2: Acts of war

Climate change insurance policies typically exclude coverage for events that are caused by acts of war. This is because acts of war are considered to be outside of the control of the insurance company.

-

Facet 3: Nuclear events

Nuclear events are also typically excluded from coverage under climate change insurance policies. This is because nuclear events can cause widespread damage and are difficult to predict.

-

Facet 4: Intentional acts

Climate change insurance policies do not cover events that are caused by intentional acts. This means that if you intentionally damage your property, your insurance company will not cover the costs.

These are just a few of the most common exclusions in climate change insurance policies. It is important to read your policy carefully to understand what is and is not covered.

Insurers

As the effects of climate change become more severe, more and more insurance companies are offering climate change insurance. This type of insurance can provide coverage for a variety of climate-related events, such as hurricanes, floods, wildfires, and sea level rise.

-

Facet 1: Growing demand

The demand for climate change insurance is growing as businesses and homeowners become more aware of the risks posed by climate change. This is leading to a number of insurance companies offering climate change insurance products. -

Facet 2: Different types of coverage

Climate change insurance policies can vary in terms of the coverage they provide. Some policies only cover specific types of events, such as hurricanes or floods, while other policies provide more comprehensive coverage. -

Facet 3: Costs and availability

The cost of climate change insurance will vary depending on the type of coverage and the location of the property. Climate change insurance is not yet available in all areas, but it is becoming more widely available. -

Facet 4: Future of climate change insurance

The future of climate change insurance is bright. As the demand for this type of insurance grows, more and more insurance companies are expected to offer climate change insurance products.

Climate change insurance is a valuable tool that can help businesses and homeowners protect themselves from the financial impacts of climate change. As the effects of climate change become more severe, more and more people are turning to climate change insurance for peace of mind.

Availability

The availability of climate change insurance varies depending on the location. In areas that are at high risk for climate change-related events, such as hurricanes, floods, and wildfires, climate change insurance is more likely to be available. However, in areas that are at low risk for climate change-related events, climate change insurance may not be available or may be very expensive.

The availability of climate change insurance is important because it can help businesses and homeowners protect themselves from the financial impacts of climate change. Climate change-related events can cause extensive damage to property and infrastructure, and the costs of rebuilding and repairing can be significant. Climate change insurance can help to cover these costs and provide financial peace of mind.

If you are considering purchasing climate change insurance, it is important to check with your insurance company to see if it is available in your area. If it is not available, you may want to consider other options for protecting yourself from the financial impacts of climate change, such as investing in flood insurance or hurricane insurance.

The following table provides a summary of the key points discussed in this section:

| Factor | Description |

|---|---|

| Availability | Varies depending on location and risk |

| Importance | Provides financial protection from climate change impacts |

| Alternatives | Flood insurance, hurricane insurance |

Benefits

Climate change insurance provides a number of important benefits to businesses and homeowners. These benefits include:

- Financial protection: Climate change insurance can provide financial protection from the costs of climate change-related events, such as hurricanes, floods, wildfires, and sea level rise. These events can cause extensive damage to property and infrastructure, and the costs of rebuilding and repairing can be significant. Climate change insurance can help to cover these costs and provide financial peace of mind.

- Peace of mind: Climate change insurance can provide peace of mind knowing that you are financially protected from the impacts of climate change. Climate change is a growing threat, and the effects are being felt around the world. By having climate change insurance, you can rest assured knowing that you are taking steps to protect yourself from the financial impacts of this global threat.

- Increased resilience: Climate change insurance can help businesses and homeowners to increase their resilience to climate change. By having insurance in place, businesses and homeowners can be more confident in their ability to recover from climate change-related events and continue operating. This can help to protect jobs, livelihoods, and communities.

The following table provides a summary of the key points discussed in this section:

| Benefit | Description |

|---|---|

| Financial protection | Covers costs of climate change-related events |

| Peace of mind | Provides assurance against financial impacts |

| Increased resilience | Enhances ability to recover and continue operating |

Risks

Not having climate change insurance can expose businesses and homeowners to a number of significant risks. These risks include:

- Financial ruin: Climate change-related events can cause extensive damage to property and infrastructure, and the costs of rebuilding and repairing can be significant. Without climate change insurance, businesses and homeowners may be forced to pay these costs out of pocket, which could lead to financial ruin.

- Business interruption: Climate change-related events can also disrupt business operations, leading to lost revenue and productivity. Without climate change insurance, businesses may not be able to recover from these disruptions, which could lead to permanent closure.

- Loss of property: Climate change-related events can also lead to the loss of property, including homes, businesses, and other structures. Without climate change insurance, businesses and homeowners may be forced to replace these losses out of pocket, which could be a significant financial burden.

The following table provides a summary of the key points discussed in this section:

| Risk | Description |

|---|---|

| Financial ruin | Climate change-related events can cause extensive damage to property and infrastructure, leading to significant financial losses |

| Business interruption | Climate change-related events can disrupt business operations, leading to lost revenue and productivity |

| Loss of property | Climate change-related events can lead to the loss of property, including homes, businesses, and other structures |

Future

As the effects of climate change become more severe, the demand for climate change insurance is expected to grow. This is because climate change is increasing the frequency and severity of extreme weather events, such as hurricanes, floods, and wildfires. These events can cause significant damage to property and infrastructure, and climate change insurance can help to cover the costs of rebuilding and repairing.

- Increased demand: The demand for climate change insurance is expected to continue to grow as the effects of climate change become more severe. This is because climate change is increasing the frequency and severity of extreme weather events, which can cause significant damage to property and infrastructure.

- New products and services: Insurance companies are developing new products and services to meet the growing demand for climate change insurance. These products and services include policies that cover a wider range of climate change-related events, as well as policies that are designed to help businesses and homeowners adapt to the effects of climate change.

- Government support: Governments are also taking steps to support the development of climate change insurance. For example, the United States government has created a program that provides grants to insurance companies that develop new climate change insurance products.

- International cooperation: Climate change is a global problem, and it will require international cooperation to address it. Insurance companies are working together to develop global climate change insurance policies that will help to protect businesses and homeowners around the world.

The future of climate change insurance is bright. As the demand for climate change insurance grows, insurance companies are developing new products and services to meet this demand. Governments are also taking steps to support the development of climate change insurance. And, insurance companies are working together to develop global climate change insurance policies that will help to protect businesses and homeowners around the world.

Frequently Asked Questions on Climate Change Insurance

This section addresses common concerns and misconceptions regarding climate change insurance, providing concise answers to empower informed decision-making.

Question 1: What is climate change insurance, and how does it differ from traditional insurance policies?

Climate change insurance is specifically designed to cover financial losses resulting from climate change-related events, such as extreme weather occurrences and sea level rise. Unlike traditional insurance policies that focus on specific perils, climate change insurance provides comprehensive protection against the evolving risks posed by climate change.

Question 2: Is climate change insurance widely available?

The availability of climate change insurance varies across regions. It is becoming increasingly accessible in areas prone to climate change impacts, but its availability may be limited in certain locations. It is advisable to consult with insurance providers to determine availability in your specific area.

Question 3: How much does climate change insurance cost?

The cost of climate change insurance depends on various factors, including the location, level of coverage, and deductible options. Premiums can vary significantly, so it is recommended to compare quotes from multiple insurance companies to find the most suitable and cost-effective policy.

Question 4: What types of events are typically covered by climate change insurance?

Climate change insurance policies typically cover a range of events resulting from climate change, such as hurricanes, floods, wildfires, droughts, and sea level rise. The specific events covered may vary depending on the policy and the insurance provider.

Question 5: What are the benefits of having climate change insurance?

Climate change insurance offers several benefits, including financial protection against climate-related losses, peace of mind knowing you are prepared for potential impacts, and increased resilience in the face of climate change challenges.

Question 6: What should I consider when purchasing climate change insurance?

When purchasing climate change insurance, it is important to carefully review the policy details, understand the coverage limits, deductibles, and exclusions. Consider your specific risks and needs, and compare different policies to find the one that best meets your requirements.

Understanding climate change insurance is crucial for mitigating the financial risks associated with climate change. By addressing common questions and providing informative answers, this FAQ section empowers individuals and businesses to make informed decisions regarding climate change insurance.

Explore further to learn about the significance of climate change insurance and its implications for safeguarding against climate-related financial losses.

Climate Change Insurance Tips

In the face of increasing climate change impacts, proactive measures are essential to safeguard financial well-being. Climate change insurance can provide a safety net against climate-related risks, and understanding how to navigate this insurance landscape is crucial.

Tip 1: Assess Your Vulnerability

Identify your location’s susceptibility to climate change-related events, such as hurricanes, floods, or wildfires. Determine the potential financial implications of these events on your property and assets.

Tip 2: Explore Coverage Options

Research different climate change insurance policies to understand the range of coverage available. Consider the types of events covered, policy limits, and deductibles that align with your specific needs and risk profile.

Tip 3: Compare Quotes

Obtain quotes from multiple insurance providers to compare premiums, coverage details, and customer service. This comparison will help you secure the most comprehensive and cost-effective policy for your situation.

Tip 4: Understand Exclusions

Carefully review the policy’s exclusions to avoid unexpected gaps in coverage. Common exclusions include gradual changes in climate patterns or events caused by human negligence.

Tip 5: Consider Long-Term Implications

Climate change is an ongoing and evolving issue. Choose an insurance provider with a proven track record and a commitment to adapting policies as climate risks change over time.

Tip 6: Review Regularly

As your circumstances and climate risks evolve, periodically review your climate change insurance policy. Adjust coverage limits, deductibles, or policy terms as needed to ensure continued protection.

Tip 7: Promote Risk Mitigation

Invest in measures that reduce your vulnerability to climate change impacts, such as flood-proofing your property or installing energy-efficient systems. This can lower your insurance premiums and enhance your overall resilience.

Tip 8: Seek Professional Advice

If you have complex insurance needs or require guidance in selecting the right climate change insurance policy, consider consulting with an insurance professional or financial advisor.

By following these tips, you can make informed decisions about climate change insurance and protect your financial interests against the increasing risks posed by climate change.

Remember, climate change insurance is a valuable tool for managing climate-related financial risks. By understanding your coverage options and taking proactive steps, you can safeguard your assets and secure a more resilient financial future.

Conclusion

Climate change insurance has emerged as a crucial tool to mitigate the financial risks associated with the escalating impacts of climate change. This exploration has shed light on the key aspects of climate change insurance, empowering individuals and businesses to make informed decisions about safeguarding their assets.

As climate change continues to reshape our world, proactive measures are essential to protect financial well-being. Climate change insurance offers a safety net against the increasing frequency and severity of climate-related events. By understanding the coverage options, assessing vulnerabilities, and implementing risk mitigation strategies, we can collectively build resilience and navigate the challenges posed by climate change.

Youtube Video:

Images References